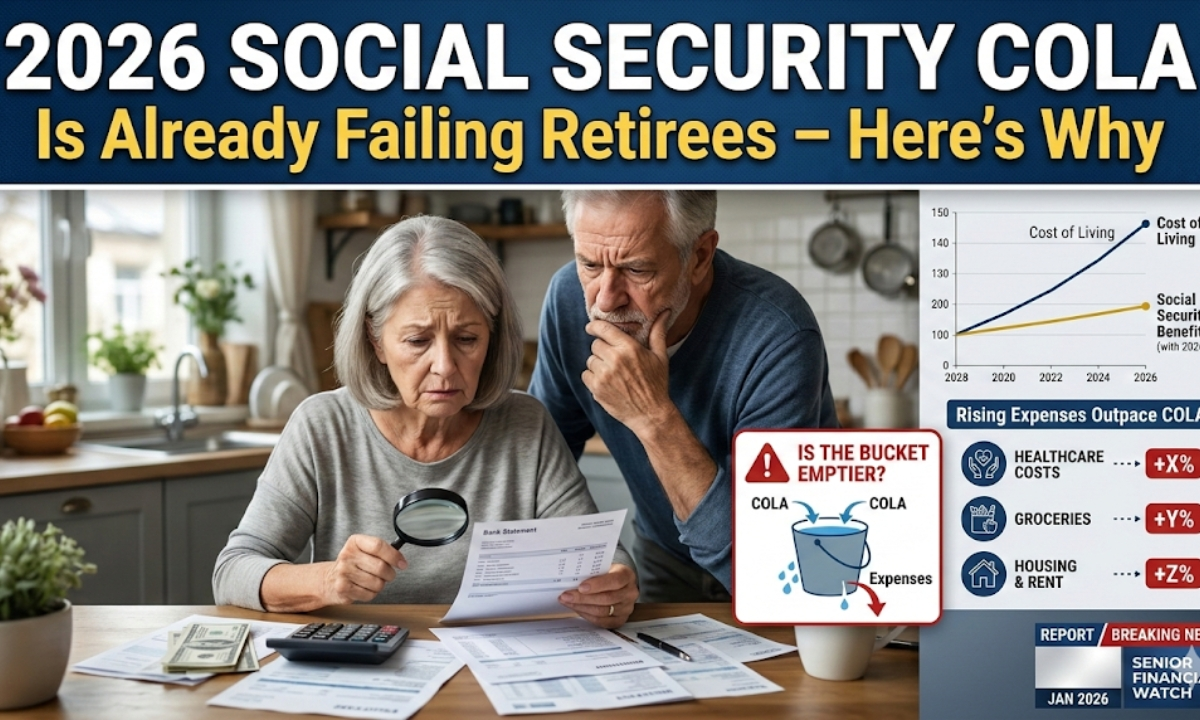

Social Security is relied upon by millions of American retirees to give their daily needs, yet even the 2.8% cost-of-living adjustment (COLA) of 2026 is not meeting expectations at the very beginning. This increase was announced late last year and will only contribute $56 more per month to the $2,015 benefit of the average retiree, raising him or her to about 2071. Though any improvements are welcome, soaring prices in housing, medical care, and food are surpassing it and leaving many wondering how they will make both ends meet just months into the year.

Inflation Beats out the Adjustment.

Each year, the Social Security Administration uses the Consumer Price Index (CPI-W), a basket of goods and services, to calculate COLA on the basis of the Consumer Price Index, Urban Wage Earners/ Clerical Workers. In the case of 2026, the data of the third quarter in 2025 indicated an increase in 2026 by 2.8 percent, compared with 3.2 percent in 2025 and the decade average of around 3 percent. But inflation is even larger on seniors, with 1-2% above reported levels in form of inflation faced by older Americans since they spend more on health care and housing, which spurred to 5-7% in early 2026.

In high-cost states such as California or New York, retirees complain of utility bills increased 12 percent and rents rising on average 4.5 percent, biting into the small increase of COLA in weeks. One of the retirees told of the fact that with the increasing property tax and food prices now 6 per cent. higher than before, her $1,900 check is barely enough to pay the bills. This imbalance causes the fixed-income households to lose purchasing power, which compels them to make such difficult decisions as not taking drugs or reducing heating.

Gains that have been gained are wiped out in Medicare Premiums.

The biggest offender is the Medicare Part B premiums that have increased 9.7 to 202.90 per month in 2026 and is imposed directly on the majority of the Social Security payment. The $56 COLA boost disappears practically overnight on the average retiree after this blow, and reduces net income by a factor of 70 among 70 percent of the beneficiaries joining the program. Medical expenses which are estimated to increase 8% in total this year take up 15-20% of retiree budgets, which is way higher than the CPI-W expects.

Benefit Type 2025average monthly 2026average monthly COLA Increment Medicare B Impact (Net)

| Benefit Type | 2025 Average Monthly | 2026 Average Monthly | COLA Increase | Medicare Part B Impact (Net) |

|---|---|---|---|---|

| Retirement | $2,015 | $2,071 | +$56 | ~$0 to -$10 |

| Spousal | $954 | $981 | +$27 | ~$0 |

| Survivor | $1,575 | $1,619 | +$44 | -$10 to -$20 |

| Disability | $1,583 | $1,627 | +$44 | ~$0 to -$10 |

According to the SSA data, this table indicates the neutrality of premiums on the majority of people regarding COLA. The squeeches are no better on the spouses and survivors, and out-of-pocket drug payments have already increased by another $50-100 per month to many.

Everyday Costs Hit Hardest

Groceries and energy prices are not cooling down, and eggs are 15% and natural gas 10% more expensive under the pressure of supply chain issues and weather conditions. This is experienced acutely by retirees, who do use 30 percent of their income on food and utilities compared to 13 percent of workers, where a $200 grocery bill now costs $215, half the COLA in a month. Home burdens also become worse with 40 per cent of the elderly having houses that are not mortgaged but wrestling with rising home repairs and insurance costs that have soared by 20%.

Stable mortgage payments are more cumbersome since property taxes have increased 5-8 percent in most locations.

Homeowners insurance was averaged at 2,500 annually, which is a raise of 2,100, and it is straining the budgets.

Driving expenses such as gas price at 3.60-gallon mean an extra 20-30 a month costs.

These unseen costs make the COLA a mirage that makes 25% of retirees raid savings or find part-time employment as recent surveys indicate.

Problems of Long-term Trust Develop.

The formula used to calculate the COLA since 1975 has not changed since then, basing on the broad CPI-W data, which underestimates seniors-specific inflation, causing the advocacy groups such as AARP to demand a Senior CPI. This archaic approach, critics say, has lost 20 per cent of the benefits in real terms over 15 years, creating a sense of mistrust in the system when solvency warnings are being sounded -the trust fund can run out in 2034 without reforms. The administration of President Trump has made pledges of review but the news that this might not be resolved soon comes early in 2026.

Retirees are also concerned about future cuts with those who claim early at 62 years old and whose value is reduced permanently by 30 percent being better off by claims at full retirement age (67 years). The payment increases of 24 by delaying to 70, a strategy that is gaining momentum because COLA is no longer reliable.

Steps Retirees Can Take Now

To offset the deficit, professionals encourage having as many benefits as possible: work more hours when you can, arrange spousal benefits, or consider Roth conversions to pay less taxes. Senior centers and other community-based resources provide food support, and reverse mortgages provide housing assistance, but sparingly, with fees. The development of personal inflation through apps creates awareness and the need to adopt CPI-E might transform future COLAs.

FAQs

Q1: What is the Social Security COLA rate in 2026?

It stands at 2.8 per cent, which contributes approximately 56 dollars to the average retirement benefits.

Q2: Why does Medicare lower my COLA earning?

Part B premiums increased to 202.90, which was usually being subsidized by direct deductions.

Q3: What can pensioners do to lengthen their pensions?

Wait until 70, reduce unnecessary spending, and spend with assistance programs on food or utility.