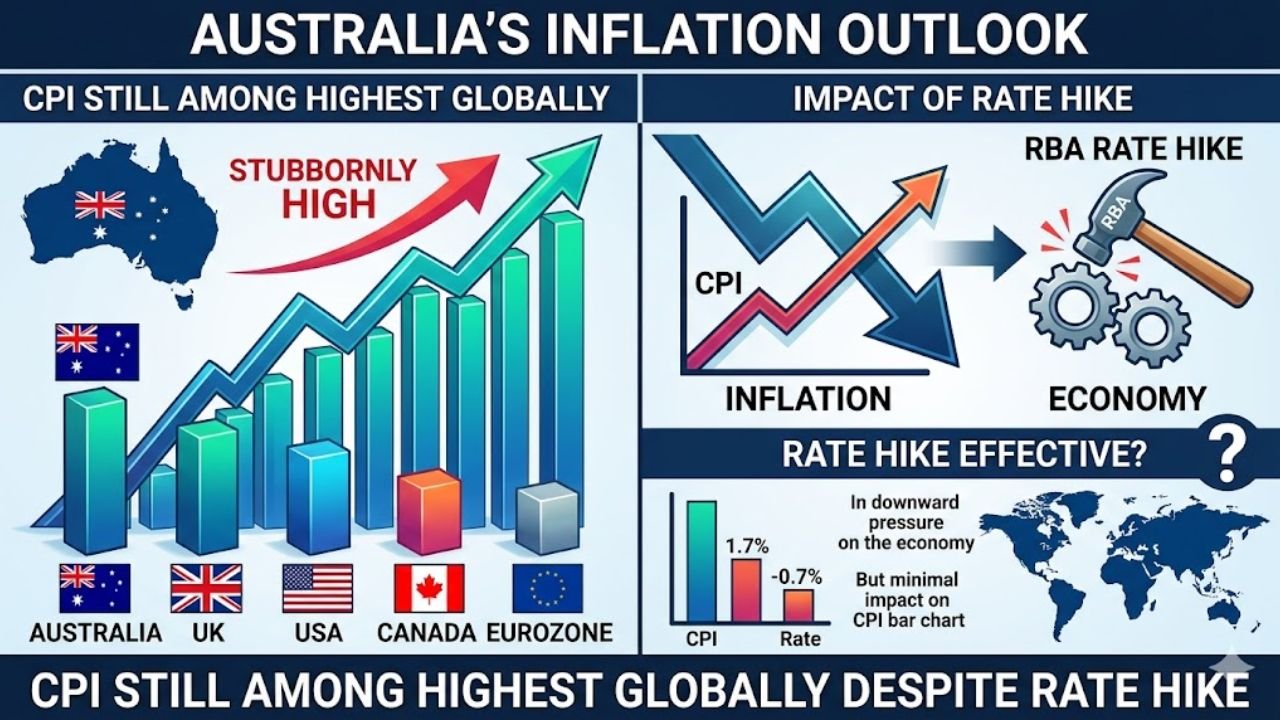

The Australian economy in 2026 continues to face significant challenges. Despite strict monetary policies, inflation remains elevated compared to other developed nations. Australia’s headline inflation stands at 3.8%, while many advanced economies are nearing their 2% targets.

In March 2026, the Reserve Bank of Australia (RBA) raised the official cash rate to 4.10%, reflecting growing concerns over persistent domestic inflation pressures. The decision revealed internal divisions within the board, highlighting the complexity of balancing inflation control with economic growth.

The Restlessness of Domestic Price Pressures

Australia’s inflation is largely driven by internal factors. The housing market has seen annual inflation rise to 6.8%, fueled by strong migration, housing shortages, and rising rents. These pressures continue to push overall inflation higher.

Additionally, the removal of federal and state energy rebates has led to a surge in electricity costs, rising over 32% annually. This has placed significant strain on household budgets.

Unlike the global trend of goods disinflation, Australia is experiencing strong services inflation. Wage growth and resilient consumer spending in sectors like dining and entertainment are keeping demand elevated.

Global Inflation Comparison

Country/Region

Headline CPI

Policy Rate

Australia

3.8%

4.10%

United States

3.2%

5.25% – 5.50%

United Kingdom

3.0%

5.25%

Euro Area

1.9%

4.00%

Canada

1.8%

4.50%

While most developed economies are nearing inflation targets, Australia remains an outlier, forcing the RBA to maintain a hawkish stance.

The RBA’s Balancing Act

The narrow board vote on the recent rate hike highlights the difficulty of current policy decisions. The RBA is focused on the output gap — the difference between economic demand and supply capacity.

Although some retail sectors show signs of slowing, Australians continue spending heavily on services. The RBA expects inflation to return to its 2–3% target range only by early 2027.

Geopolitical and Energy Risks

Global uncertainties, particularly in the Middle East, pose additional risks. Rising oil prices could increase import costs, especially for energy-dependent economies like Australia.

If energy prices continue to rise, the RBA may implement further rate hikes, potentially leading to prolonged cost-push inflation and slower economic growth.

Future Outlook: A Long Road to Stability

The Australian economy is expected to experience below-trend growth as higher interest rates begin to affect household incomes and business investment.

With unemployment at a low 4.1%, the labor market remains tight. However, rising borrowing costs may reduce business activity in the coming months.

The upcoming CPI data release in April 2026 will be crucial. If inflation remains elevated, Australia may face a prolonged period of “higher for longer” interest rates.

FAQs

Q1 What causes inflation in Australia?

Inflation in Australia is mainly driven by housing shortages, rising energy costs following subsidy removal, and strong demand in the services sector.

Q2 What is the projection for interest rates in 2026?

Financial markets and major banks expect a strong possibility of another rate hike in May 2026, depending on inflation trends and global energy prices.

Q3 When will inflation return to the target range?

The RBA expects inflation to return to the 2–3% target range by early 2027, though this depends on both domestic and global economic conditions.