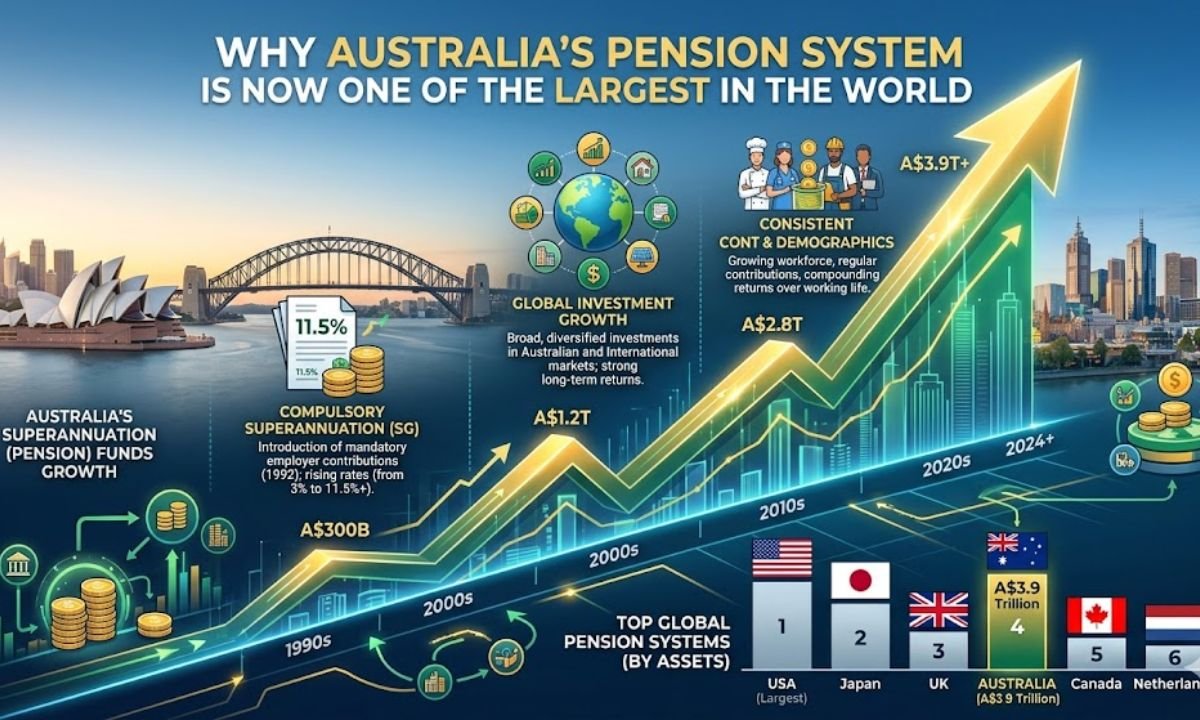

Considering its relatively small population, it is impressive that Australia is home to one of the largest pools of pension assets in the world. This phenomenon was not random. It was the result of a bipartisan policy shift to a defined contribution model known as Superannuation.

Implemented in the early 1990s, the system shifted retirement funding from the state to a shared responsibility model between employers and employees. Rather than relying solely on government pensions, each employee’s income is legally required to contribute to a state-regulated investment fund.

Superannuation has become a self-sustaining engine of capital that is projected to reach $3.9 trillion AUD as the contribution rate approaches its 12% target. This enormous pool of savings not only secures the financial future of millions of Australians but also positions Australia as a major player in global capital markets.

The Magnitude of the Superannuation Guarantee and Compounded Growth

The Superannuation Guarantee (SG) is the core driver behind Australia’s retirement success. Unlike many developed countries that rely on voluntary or tax-incentivized retirement savings programs, Australia’s system is compulsory.

Employers must contribute a percentage of an employee’s salary into their nominated superannuation fund. As a result, every employee accumulates retirement savings automatically.

This automatic investment structure offers several advantages:

- Regular contributions regardless of economic conditions

- Long-term compounding investment growth

- Diversified exposure to global assets

- Reduced reliance on government pensions

Because funds remain locked until retirement age, investment managers can allocate capital toward long-term projects such as infrastructure, airports, renewable energy developments, and global private markets. These investments often generate higher long-term returns than traditional stock and bond portfolios.

This structure also benefits the broader Australian economy by ensuring a steady domestic capital flow that supports national development.

Pension Assets as a Percentage of GDP

The following table illustrates how Australia’s pension assets compare globally as a share of GDP.

| Country | Pension Assets (% of GDP) | Primary System Type |

|---|---|---|

| Australia | 175% | Compulsory Defined Contribution |

| USA | 160% | Mixed (Social Security / Voluntary) |

| UK | 125% | Mixed (State / Auto-enrolment) |

| Canada | 155% | Mixed (CPP / Private) |

| Netherlands | 210% | Quasi-Mandatory Occupational |

Australia’s pension assets exceed 175% of GDP, placing it among the largest retirement systems in the world relative to economic size.

Governance and the Rise of Mega-Funds

Over the past decade, Australia’s superannuation industry has experienced significant consolidation. Regulatory oversight from the Australian Prudential Regulation Authority (APRA) has increased performance standards and transparency.

This has led to mergers among industry and retail funds, creating massive investment institutions. Funds such as AustralianSuper and Australian Retirement Trust now manage hundreds of billions of dollars.

The scale of these mega-funds allows them to:

- Invest directly in global infrastructure

- Access private markets

- Reduce investment management costs

- Improve returns for members

Industry funds also operate as profit-to-member organizations, meaning investment gains are returned directly to members rather than external shareholders.

Economic Resilience and the Future of the Silver Economy

Australia’s population is steadily aging, and the superannuation system is transitioning from the accumulation phase to the decumulation phase. This means increasing numbers of retirees will begin withdrawing funds.

Despite this shift, the system continues to play a crucial role in national wealth generation.

Recent policy initiatives such as the Retirement Income Covenant require super funds to develop strategies that help retirees manage their savings throughout retirement.

The goal is no longer simply building retirement balances but ensuring retirees maintain financial stability and a dignified standard of living.

Additionally, the vast pool of superannuation capital provides Australia with a form of economic sovereignty. Super funds are major shareholders in domestic companies and key financiers of infrastructure projects.

This reduces fiscal pressure on the taxpayer-funded Age Pension while allowing individuals to maintain personal retirement wealth.

Global Influence and the Export of the Australian Model

Australia’s superannuation framework has attracted growing international attention. Global policy institutions frequently cite it as a potential model for countries facing demographic challenges such as aging populations and shrinking workforces.

Unlike many systems that rely heavily on government funding, Australia’s approach ensures retirement savings are invested and grown within individual accounts.

As a result, the system not only supports retirees but also strengthens Australia’s financial ecosystem, helping it withstand global economic volatility.

FAQs

Q1 What is the current Superannuation Guarantee rate in Australia?

For the fiscal years 2025–2026, the Superannuation Guarantee rate is 11.5%. It is scheduled to increase to 12% on July 1, 2026.

Q2 Do Australians get a say in how their pension funds are invested?

Yes. Most Australians can choose their superannuation fund and select investment strategies ranging from conservative cash portfolios to high-growth equity funds and sustainable investment options.

Q3 What makes the Australian system different from the US Social Security system?

The United States primarily uses a pay-as-you-go Social Security system funded through taxes. Australia’s superannuation system is fully funded, meaning retirement savings are invested in individual accounts and grow over time for the benefit of each account holder.